Conflicting currents are buffeting the markets, and it’s difficult to see the clear path forward for investors. The falling rate of annualized inflation and the continued resilience of the jobs market point toward continued economic strength – but interest rates are high, oil prices are rising, and the dollar is strong, which all tend to signal economic trouble.

Until recently, the conventional wisdom has favored a ‘soft landing,’ with the Fed’s higher rates bringing down inflation, and permitting economic conditions to normalize without undue ripple effects. Lately, however, sentiment has been shifting. Noted economist Mohamed El-Erian lays out the reasons why he has come around to a more pessimistic view, and predicts troubled economic times ahead.

“For well over a year now, I have argued that the US is able to avoid the 2023 recession that many were repeatedly calling. I am now less confident about what’s in store for 2024… An intense period of rising interest rates, high oil prices and a stronger dollar is pushing the financial market consensus on US economic growth away from the comforting notion of a soft landing… These are developments that the economy and markets do not enjoy. They damp growth and increase the threat of stagflation,” El-Erian opined.

If El-Erian is right, and the US economy is heading toward trouble, investors should start playing defense and shifting resources toward dividend stocks, the classic defensive play. These shares assure a return through passive income, no matter how the markets turn – and when they get a ‘Strong Buy’ rating from the Street’s analysts, that’s a clear sign that investors should take notice.

We used the TipRanks platform to look at the details on two such stocks, both with dividend yields above 7% and Strong Buy ratings.

Enterprise Products Partners (EPD)

The first ‘Strong Buy’ dividend stock on our list is Enterprise Products Partners, a midstream company in the North American energy sector. With a market cap of $58 billion, Enterprise is one of the continent’s largest midstream players and one of the largest public partnerships in the Wall Street trading markets.

The midstream sector is a vital component in hydrocarbon production and distribution; midstreamers move the product from the wellheads and production regions to storage facilities, refineries, and distribution nodes. Enterprise operates a continent-spanning network of oil and gas transportation assets, including 50,000 miles worth of pipelines, 25 fractionation facilities, 20 deepwater docks, and storage assets capable of holding more than 260 MMBbls of liquids. This network is centered in the Texas-Louisiana coastal region and branches out to the Southeast, Appalachia, the Mississippi Valley, and northwest to the Rocky Mountains.

These operations are profitable, and Enterprise generated $10.65 billion at the top line in its last reported quarter, 2Q23. That result, however, was down more than 33% year-over-year and missed the forecast by $1.67 billion. At the bottom line, Enterprise realized a quarterly EPS of 57 cents, a penny below the estimates. The company’s distributable cash flow also fell year-over-year, from $2.02 billion to $1.74 billion.

Despite these year-over-year declines, Enterprise has still kept up its strong dividend. The company released its most recent dividend declaration on October 5, for a 50 cent payment per common share. This dividend annualizes to $2, and at that rate yields 7.5%. Enterprise has a 24-year history of maintaining regular dividend payments and making regular increases to those payments – solid attributes for a defensive portfolio addition.

Covering this stock for Truist, 5-star analyst Neal Dingmann is impressed by the company’s ambitious plans for expansion, and its consequent potential to maintain profits.

“Enterprise sits in an enviable position with $4.1B growth projects under construction including $1.1B anticipated to begin service this year. We forecast the growth projects along with solid forecasted organic growth along with minimal incremental capital spend will lead to notable future earnings/DCF growth. The far-reaching projects with material scale puts the company in a position to weather periods of commodities pricing pressure while also able to benefit as activity/volumes grow. We forecast EPD to continue to add flex capacity where/ when appropriate such as the Beaumont Export Terminal to continue to drive future upside,” Dingmann commented.

Dingmann goes on to give EPD shares a Buy rating – along with a $33 price target that suggests the stock will gain 22.5% in the next 12 months. Add in the dividend yield, and the stock’s total yield on the one-year time frame climbs as high as 30%. (To watch Dingmann’s track record, click here)

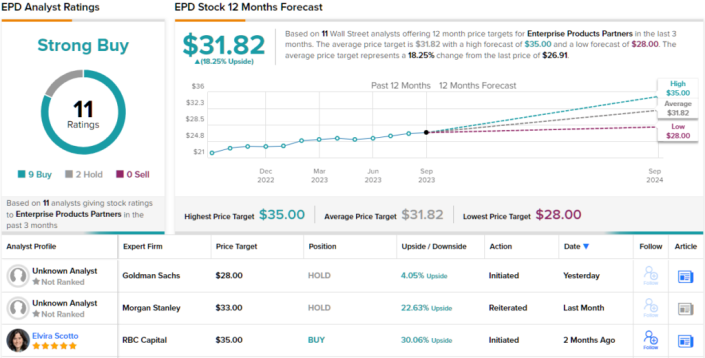

Overall, the 11 recent analyst reviews on EPD include 9 Buys and 2 Holds, to support the Strong Buy consensus rating. The shares are priced at $26.90, and their $31.82 average target price implies a one-year gain of 18%. (See EPD stock forecast)

Blue Owl Capital (OBDC)

Next up is a business development corporation, Blue Owl Capital. This firm was formed through a SPAC transaction during 1H 21 when Owl Rock and Dyal Capital together merged with Altimar Acquisition. The combined entity has since shifted its assets, operations, and branding to the Blue Owl name, and now operates under the larger umbrella of the Blue Owl Capital asset management company.

Blue Owl Capital invests in debt and equity of small- to mid-sized businesses. These investments make capital and financial services available to entrepreneurial firms that won’t necessarily qualify for such services from the traditional commercial banking system. Blue Owl’s business development corporation portfolio contains investments in 187 companies and has a fair value size of $12.9 billion. Of the total investments, 98% are floating rate, and 83% of the total are first or second lien senior secured instruments.

We’ll see Q3 results from Blue Owl on November 8, 2023, but for now, we can look back at the company’s 2Q23 results to see where it stands. On the macro level, Blue Owl brought in $394.2 million in net investment income, a result that was up more than 44% year-over-year and beat the forecast by over $10.4 million. At the bottom line, the company realized an NII of 48 cents per share, 2 cents per share better than had been anticipated.

These results supported Blue Owl’s most recent dividend declaration of 33 cents per share for an October 13, 2023, payment. The regular dividend is supplemented by a special dividend payment that was sent out last month, at 7 cents per share, the fourth consecutive quarterly supplemental payment the company has sent out. The regular dividend annualizes to $1.32 per common share and yields 10%; with the supplemental payment included in the calculation, the forward yield rises to an impressive 12%, more than enough to provide a significant level of portfolio protection.

This stock – particularly its high return generation – has caught the eye of Compass Point’s 5-star analyst, Casey Alexander, who writes of it, “The consistency of return generation at OBDC should generate more enthusiasm from investors. Over the last four quarters, NAV is up $0.78 per share, and — counting distributions — OBDC has generated a solid double-digit return on NAV. OBDC still has levers to pull to generate an incremental return, such as increased churn in the portfolio increasing fee income, and additional dividends from off-balance sheet equity vehicles. The basic earnings power is expressed in the base dividend and another increase in the special distribution. As such, we believe the upside potential and total return potential for OBDC are compelling, and we urge investors to take advantage of the current unwarranted discount to NAV.”

Looking forward, Alexander gives OBDC shares a Buy rating with a $16.50 price target that implies ~24% one-year upside potential. (To watch Alexander’s track record, click here)

All in all, the Strong Buy consensus rating on OBDC stock is based on 8 recent analyst reviews, which break down to 7 Buys and 1 Sell. The stock has an average target price of $15.59, suggesting that it will appreciate ~17% from current trading price of $13.33. (See OBDC stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

© OfficialAffairs